Worked example

Irreversible Investment — model_irrcap

This example, the first in the paper, applies OccBin to an RBC model

in which investment cannot fall below a fixed fraction of its steady-state

level. It illustrates the complete workflow: two .mod files,

a constraint string, a shock sequence, and the resulting IRF chart.

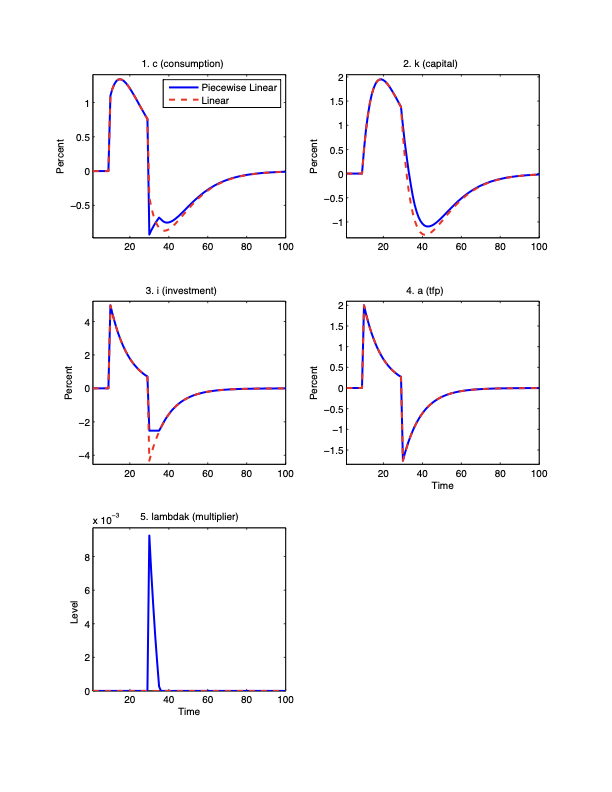

Impulse responses to a positive TFP shock at period 10 and a negative shock at period 30. Blue: piecewise-linear (OccBin). Red: linear (ignoring constraint). When investment is forced to its floor, the piecewise solution diverges sharply from the linear one.

The model and its constraint

The model is a standard RBC model with a capital adjustment cost

(PSI) and a Lagrange multiplier lambdak

on the investment floor. In the reference regime

(constraint not binding), the multiplier is zero: lambdak = 0.

In the alternative regime (constraint binding),

investment is pegged to its lower bound:

i = log(PHII · ISS).

The occasionally binding constraint is It ≥ φ · Iss, or in log-deviation form: ĩt ≥ log(φ). The constraint is violated — and regime switches — when the linear solution produces investment below this floor.

Variables in both .mod files:

| Variable | Description |

|---|---|

| a | Total factor productivity (log) |

| c | Consumption (log) |

| i | Investment (log) |

| k | Capital (log, end of period) |

| kprev | Lagged capital, defined as k(-1) |

| lambdak | Lagrange multiplier on the investment floor |

The two .mod files

The reference file dynrbc.mod sets

lambdak = 0 (equation 4 below). The alternative

file dynrbcirr_i.mod is an exact replica except

that equation 4 is replaced by

i = log(PHII · ziss), enforcing

the investment floor. All other equations and the parameter list

are identical.

// dynrbc.mod — reference regime (constraint not binding)

var a, c, i, k, kprev, lambdak;

varexo erra;

parameters ALPHA, DELTAK, BETA, GAMMAC, RHOA, PHII, PHIK, PSI, PSINEG, ISS, KSS;

model;

// 1. Euler equation (capital)

-exp(c)^(-GAMMAC)*(1+2*PSI*(exp(k)/exp(k(-1))-1)/exp(k(-1)))

+ BETA*exp(c(1))^(-GAMMAC)*((1-DELTAK)

-2*PSI*(exp(k(1))/exp(k)-1)*(-exp(k(1))/exp(k)^2)

+ALPHA*exp(a(1))*exp(k)^(ALPHA-1))

= -lambdak + BETA*(1-DELTAK+PHIK)*lambdak(1);

// 2. Resource constraint

exp(c)+exp(k)-(1-DELTAK)*exp(k(-1))+PSI*(exp(k)/exp(k(-1))-1)^2

= exp(a)*exp(k(-1))^ALPHA;

// 3. Investment definition

exp(i) = exp(k)-(1-DELTAK)*exp(k(-1));

// 4. Reference regime: multiplier is zero

lambdak = 0;

// 5. TFP process

a = RHOA*a(-1) + erra;

kprev = k(-1);

end;// dynrbcirr_i.mod — alternative regime (investment at floor)

// Identical to dynrbc.mod except equation 4:

// 4. Alternative regime: investment is pinned to its lower bound

i = log(PHII*ziss);var, varexo,

and parameters declaration must appear in the same order

in both files. Only the binding-regime equation changes.

Parameter values

Parameter values are set in paramfile_dynrbc.m,

loaded by the Dynare steady-state file at parse time.

BETA = 0.96; % discount factor

ALPHA = 0.33; % capital share

DELTAK = 0.10; % depreciation rate

GAMMAC = 2; % inverse elasticity of substitution

RHOA = 0.9; % TFP persistence

PHII = 0.975; % investment floor as fraction of I_ss

PSI = 0; % capital adjustment cost (zero here)The toolkit computes steady-state capital and investment from these primitives: Kss = ((1/β − 1 + δ) / α)1/(α−1), Iss = δ Kss.

Setting up and calling the solver

The script runsim_irrcap.m specifies the shock

sequence and calls solve_one_constraint. Here,

a positive 2% TFP shock hits at period 10 and a symmetric

negative shock at period 30, over a 100-period horizon.

clear

global M_ oo_

modnam = 'dynrbc'; % reference regime .mod file

modnamstar = 'dynrbcirr_i'; % alternative regime .mod file

% Constraint string (in deviation from steady state)

constraint = 'i<log(PHII)'; % switch to alt. regime when i hits floor

constraint_relax = 'lambdak<0'; % return to ref. regime when multiplier goes negative

irfshock = char('erra'); % TFP innovation

shockssequence = zeros(60,1);

shockssequence(10) = 0.02; % positive shock at period 10

shockssequence(30) = -0.02; % negative shock at period 30

nperiods = 100;

maxiter = 10;

[zdatalinear, zdatapiecewise, zdatass, oobase_, Mbase_] = ...

solve_one_constraint(modnam, modnamstar, ...

constraint, constraint_relax, ...

shockssequence, irfshock, nperiods, maxiter);Unpacking and plotting results

After the solver returns, the script unpacks the output arrays

into named workspace variables using a loop over the endogenous

variable list, then calls makechart to plot

piecewise-linear and linear paths side by side.

% Unpack all endogenous variables from the output matrices

for i = 1:Mbase_.endo_nbr

eval([Mbase_.endo_names{i}, '_l = zdatalinear(:,i);']);

eval([Mbase_.endo_names{i}, '_p = zdatapiecewise(:,i);']);

eval([Mbase_.endo_names{i}, '_ss = zdatass(i);']);

end

% Build chart inputs

titlelist = char('c (consumption)','k (capital)','i (investment)', ...

'a (tfp)','lambdak (multiplier)');

ylabels = char('Percent','Percent','Percent','Percent','Level');

legendlist = cellstr(char('Piecewise Linear','Linear'));

line1 = 100*[c_p, k_p, i_p, a_p, (lambdak_p + lambdak_ss)/100];

line2 = 100*[c_l, k_l, i_l, a_l, (lambdak_l + lambdak_ss)/100];

makechart(titlelist, legendlist, '', ylabels, line1, line2)lambdak turns positive during the

binding episodes, signalling that the constraint is active.